Estimated reading time: 8 minutes

When it comes to investing, timing can be everything.

But what happens if a great opportunity comes your way, and you don't have the capital to seize it? That's where financing becomes essential.

Many investors have traditionally turned to mortgage loans for seizing on opportune real estate ventures. However, there is an intriguing alternative worth exploring: non-recourse financing.

This unique financial tool can afford much-needed leverage without the need for additional collateral. It allows qualifying investors to bolster their portfolios with valuable properties that would otherwise be out of reach.

In this blog post, we'll delve into the pros and cons of non-recourse financing and highlight the steps you can take to secure a non-recourse loan for your portfolio.

Table of Contents

- Understanding Traditional Financing

- What is Non-Recourse Financing?

- 3 Benefits of Non-Recourse Financing

- Unlock Your IRA’s Real Estate Investing Potential

- Things to Consider Before Taking on a Non-Recourse Loan

- Securing Non-Recourse Financing for Your SDIRA

- Maximize Your SDIRA’s Potential with Non-Recourse Financing

Understanding Traditional Financing

With traditional loans, such as mortgages or personal loans, lenders typically assess your creditworthiness, assets, and financial history. If you default on a traditional loan, your lender can not only seize the collateral but also come after your personal assets if the collateral doesn't cover the debt.

What is Non-Recourse Financing?

In non-recourse financing, if the borrower defaults, the lender's only source of repayment is the collateral securing the loan. In other words, the lender cannot pursue the borrower's personal assets or income beyond the collateral provided for the loan.

This type of financing is commonly used to finance commercial properties or large real estate developments. If the borrower defaults, the lender can take ownership of the property but typically cannot go after the borrower's personal assets.

Non-recourse financing can offer borrowers some protection in the event of a business or investment downturn. However, non-recourse lenders often require higher collateral and higher interest rates due to the increased risk they assume.

For instance, let’s say you want to purchase a $500,000 duplex, but you only have $250,000 in cash. You can either apply for a traditional home loan, putting your personal assets on the line if you experience foreclosure. Alternatively, you can apply for a non-recourse loan, as long as you can convince a lender that the condo has sufficient income potential.

Typically, non-recourse loans require a much greater down payment than the traditional mortgage down payment of 20%. There’s less upside for the lender on this type of loan, so they want extra assurance that they’ll be able to recoup their capital.

3 Benefits of Non-Recourse Financing

Non-recourse loans offer several compelling advantages:

Potential for Higher Returns

By harnessing the power of non-recourse loans, you have the potential to accelerate the growth of your portfolio and achieve your financial goals sooner. It's essential to manage leverage prudently. However, when used wisely, the enhanced spending power that comes with a loan can lead to significant growth.

Risk Mitigation

Non-recourse loans come with a unique safety net — they are secured solely by the asset being financed. In the event of default, all other assets remain protected. Of course, this doesn’t mean non-recourse loans are without risk. The loss of collateral could mean saying farewell to a significant chunk of your portfolio.

Opens the Doors for Portfolio Diversification

Diversification is a cornerstone of many long-term investment strategies. Yet, with record-high real estate prices, a single direct purchase may drain most of the capital from your portfolio, leaving little room to invest in other assets.

Taking out a non-recourse loan may allow you to retain more liquidity for investments beyond real estate. For example, with the capital you save by taking out a non-recourse loan, you can explore opportunities in other asset classes like precious metals, cryptocurrency, and private equity.

Unlock Your IRA’s Real Estate Investing Potential

Many savvy investors are still unaware that the IRS permits investing in real estate with your retirement funds. You most likely can’t do this with an IRA at your existing bank or brokerage. They don’t have the infrastructure or expertise to administer alternative assets.

Instead, you’ll need a self-directed IRA (SDIRA).

These accounts are exactly the same as all other IRAs, with one distinct advantage: your investment options are nearly limitless.

With an SDIRA administrator, you’re not limited to traditional stocks and bonds. Instead, you can expand your portfolio with alternative assets, including real estate.

5 Steps to investing in Real Estate with an SDIRA. Get your free copy now >

Given the median home price of around $430,000, many account holders may not have the requisite funds for a direct purchase. Fortunately, adding funds to your SDIRA is simple. You can transfer or rollover funds from another IRA or an inactive employer-sponsored plan like a 401(k).

You may also contribute funds directly to these accounts. Here's the catch – these accounts are subject to annual contribution limits. For 2024, you can contribute up to $7,000, or $8,000 if you're over 50.

Fortunately, transfers, rollovers, and contributions aren’t the only way to increase your budget.

In addition to non-recourse loans, investors can also consider partnering, a powerful investment strategy to amplify your purchasing power. Your SDIRA can join forces with others, even disqualified persons like parents and spouses, at the initial purchase stage to pool resources for a collective investment.

Can’t I Take Out A Personal Loan For My SDIRA?

No. IRA holders cannot extend their personal credit to their IRAs. In the eyes of the IRS, this qualifies as self-dealing, one of the core prohibited transactions for an SDIRA.

Your SDIRA has no credit history. The only reason your SDIRA would qualify for a traditional loan is a guarantee based on your strong personal credit history. Extending your personal credit to your IRA could result in severe tax penalties, potentially disqualifying the entire account.

So, lenders will usually only consider assets with sufficient income potential to fund a non-recourse loan. For this reason, most lenders will only extend a non-recourse loan for multifamily real estate assets as a way to mitigate risk.

Things to Consider Before Taking on a Non-Recourse Loan

While non-recourse loans may offer substantial benefits for SDIRA investors, it's crucial to approach them with a clear understanding of the potential risks involved.

Loan Terms and Interest Rates

Non-recourse loans are inherently riskier for lenders than traditional loans, so they often bring higher interest rates. These rates can vary depending on factors like the loan-to-value ratio and the prevailing market conditions.

Before signing onto any loan, it's essential to thoroughly evaluate the interest rates and terms offered by different lenders. Additionally, you should consider the potential returns from the real estate asset to ensure that the investment's profitability outweighs the cost of borrowing.

Limited Lender Options

Compared to traditional loans, non-recourse lenders are relatively fewer in number. This limited pool of lenders may result in fewer options and potentially less favorable loan terms. It's advisable to shop around and explore different lenders to find the best fit for your SDIRA investment.

We have worked with a number of non-recourse loan lenders who may be willing to take a look at your prospective investment.

Unrelated Debt-Financed Income (UDFI)

When you use a non-recourse loan to purchase an investment property within your SDIRA, you are effectively financing a portion of the investment with borrowed funds. This means that a percentage of the income generated by the property is considered debt-financed income.

Generating income by taking on debt is not the primary purpose of your IRA, according to the IRS. Therefore, this income is not tax-preferred. It’s considered unrelated debt-financed income, or UDFI.

The income attributed to UDFI is subject to unrelated business income tax (UBIT) at trust tax rates. This starts at 10% but can reach as high as 37% in the top income bracket.

How to Calculate UDFI

To calculate UDFI, you must determine the percentage of income generated by the debt-financed portion of the investment. This percentage is based on the ratio of the acquisition debt (the non-recourse loan amount) to the adjusted basis of the investment.

If your SDIRA generates UDFI, you will need to file IRS Form 990-T to report and pay any UBIT owed. The deadline for filing this form is typically April 15th of the following tax year.

It's crucial to work closely with a tax advisor or financial professional experienced in SDIRAs and UDFI to ensure compliance with tax regulations. Tax laws can change; your responsibility to adhere to them does not.

Ready to learn the ropes? Dive into our SDIRA Rules Guide

Securing Non-Recourse Financing for Your SDIRA

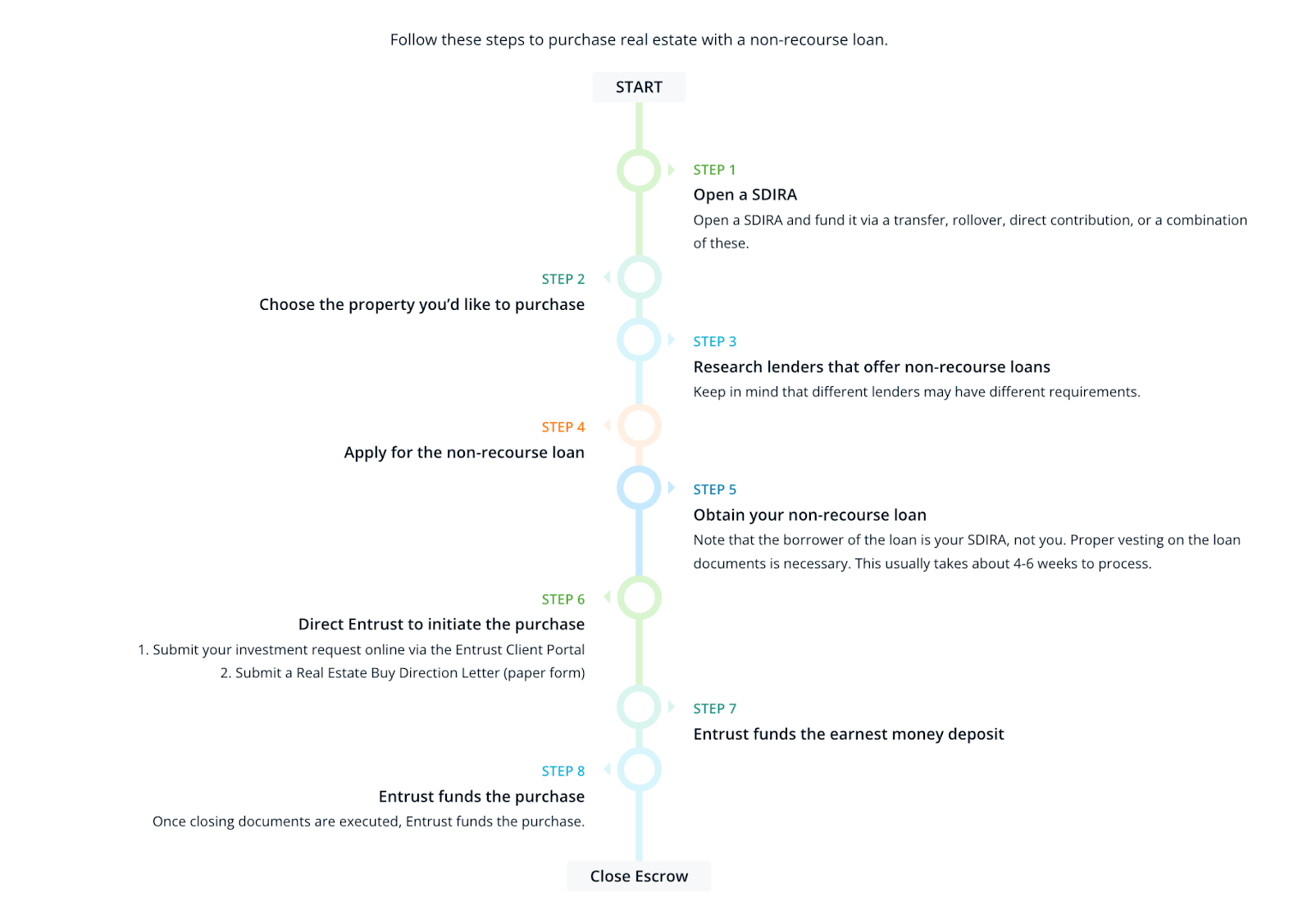

Follow these eight steps to help navigate the process of purchasing real estate in your SDIRA with a non-recourse loan:

- Open an SDIRA: Start by opening an SDIRA with Entrust and fund it through various methods like transfers, rollovers, or direct contributions.

- Choose Your Property: Select the real estate property you wish to purchase.

- Research Lenders: Explore lenders that offer non-recourse loans, considering their specific requirements.

- Apply for the Loan: Begin the application process for the non-recourse loan.

- Secure Your Loan: Remember that your SDIRA is the borrower, not you personally.

- Direct Entrust: Instruct Entrust to initiate the purchase through the Entrust Client Portal or by submitting a Real Estate Buy Direction Letter.

- Fund Earnest Money: Entrust funds the earnest money deposit on your behalf.

- Fund the Purchase: Once all closing documents are finalized, Entrust funds the purchase, and you can close escrow. That’s it!

Maximize Your SDIRA’s Potential with Non-Recourse Financing

Real estate has long been a cornerstone of investment strategies, offering stability and potential for substantial returns. However, rising property prices can make it challenging to access high-value real estate assets. Fortunately, non-recourse financing offers a strategic financial tool that can unlock new possibilities for your portfolio.

This strategy can substantially boost your IRA’s purchasing power, allowing you to explore lucrative real estate opportunities that might have seemed out of reach.

Want to learn more about how to invest in real estate with your retirement funds? Explore our Learning Center. Over the years, we’ve created countless articles, webinars, and in-depth resources outlining all things real estate, including our 5 Steps to Investing in Real Estate Guide.

Or, if you're ready to explore whether an SDIRA is right for you, connect with one of our knowledgeable SDIRA experts. They can explain more about non-recourse loans and give you the tools you need to determine if this path aligns with your investment goals.

0 Comment